Risky Business: Robinhood's 1% Cash Bonus Offer

Risky Business: Robinhood's 1% Cash Bonus Offer

A Golden Opportunity or a Crazy Gamble?

A few weeks ago, I came across this offer from Robinhood to pay a 1% cash bonus on all securities and options transferred from an existing brokerage account, before Jan 31st, 2024. On its surface, the pitch looked amazing.

I’ve been a long-time customer of Charles Schwab after first opening a brokerage account there 20 years ago as a teenager. Schwab’s customer service has always been impeccable. It’s easy to get in touch with someone on the phone, and their agents are well informed and extremely helpful. Schwab’s checking account is one of the best, and has saved me from paying exorbitant ATM fees during international travel.

Robinhood’s reputation

Conversely, my opinion of Robinhood has been mixed at best. The app has always felt more geared towards active day-traders, and seems to treat investing less as a passive activity, and more of a casino fueled by crypto trading and meme stocks. Up until recently, the only way to reach customer service was via in-app messaging with no way to directly speak to a human. The Gamestop saga and Robinhood’s cozy relationship with Citadel both left a sour taste. For a classic long-term buy-and-hold investor like myself, Robinhood’s approach feels almost antithetical to my instincts.

Nevertheless, a free 1% bonus on all assets would be a sizable sum, so I decided to dive a little deeper.

Upon closer inspection

The first place I headed was to Robinhood’s terms on the bonus. The terms make no mention of any cap on the bonus amount, but they do call out another limitation.

“Robinhood will deposit 1% of the net transferred asset value to the customer’s Brokerage Account, subject to a two-year earn-out.”

The FAQ expands on this:

“As long as you keep the eligible funds for at least 2 years in your Robinhood brokerage account, the bonus is yours to keep. If you withdraw money earlier than 2 years from when it’s settled in your account, and your remaining account balance stays at or above the net transferred value that earned the bonus, it’s yours to keep.”

Okay, back to Schwab…

Given my skepticism around Robinhood, I decided to email my advisor at Schwab and see if they would be able to offer a bonus to keep my business. I received a promising note from him the next day.

When we connected over the phone the next day, my advisor apologized and said that he was mistaken and that Schwab would not be able to match Robinhood’s offer. In his own words, “I was under the impression that the bonus was capped — I’ve never heard of an uncapped offer like Robinhood’s. If I were you, I would move to Robinhood.”

Okay, so what’s the catch?

The WSJ wrote a piece in December on Robinhood’s strategy :

The trading app received about $1.1 billion in account transfers since Oct. 23, when it began offering a 1% match on transferred brokerage accounts, the company said. In the second and third quarters of this year, customers transferred about $350 million and $375 million.

That’s nearly 3x growth in quarterly deposits since launching this offer! Given the $1.1 billion figure, Robinhood has paid out $11 million in bonuses out to customers thus far.

The WSJ expands:

Robinhood has been trying to become more than just a trading app for young, first-time investors as trading activity has dropped. The brokerage’s monthly active users have roughly halved from pandemic-era highs, while revenue from interest has eclipsed that of trading-related activities.

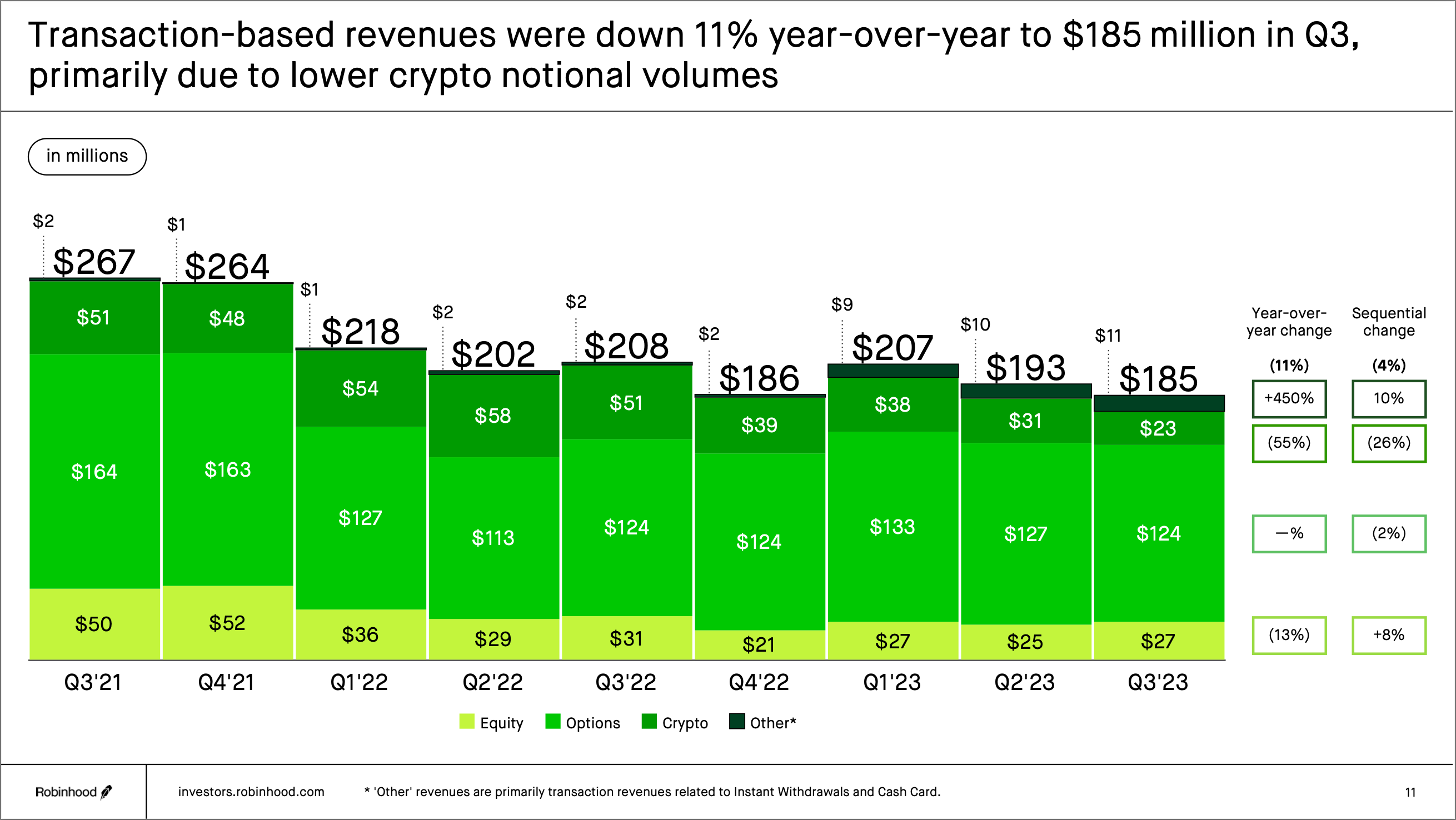

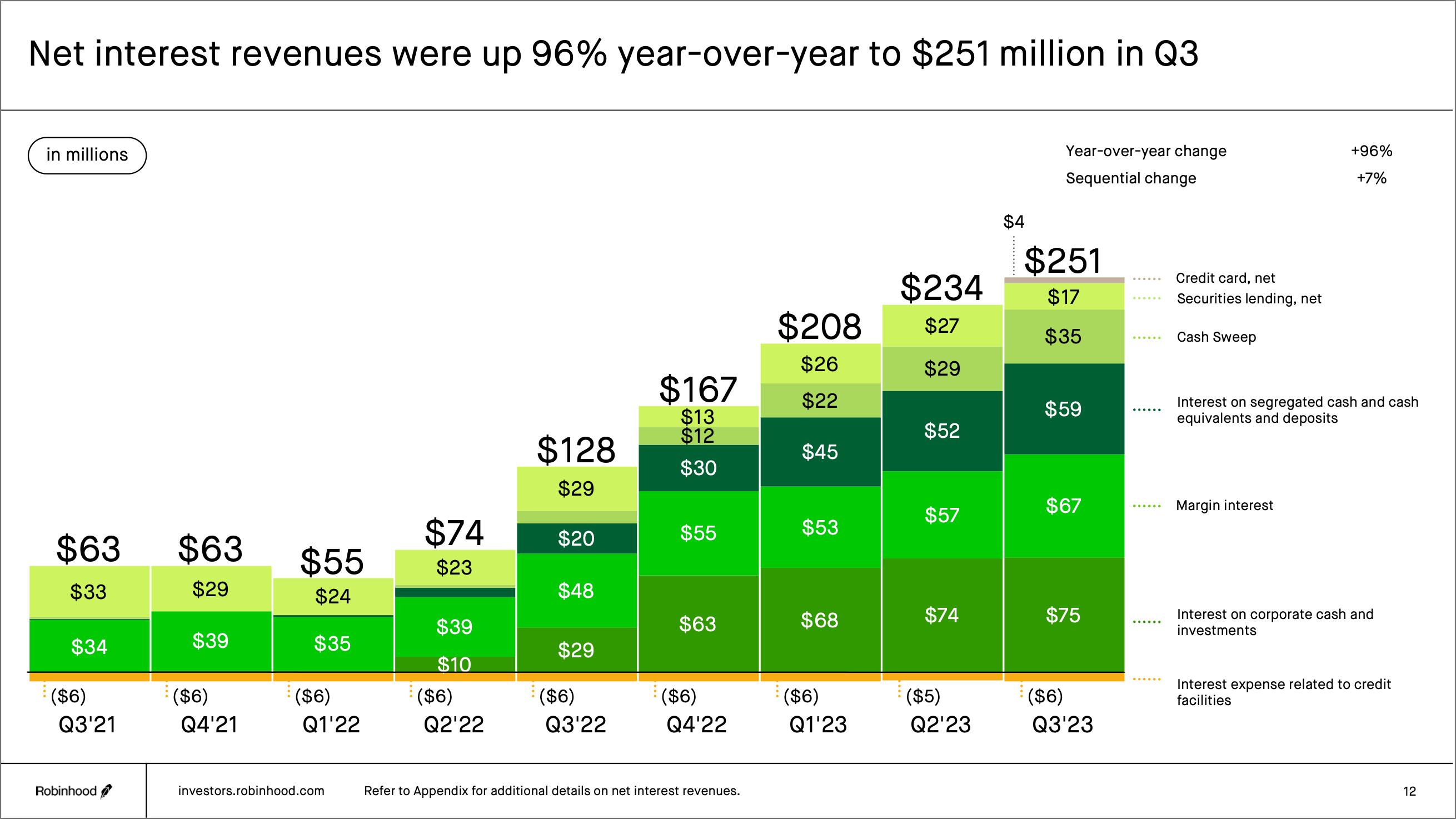

In essence, with the end of the ZIRP era, revenue from order flow and crypto trading has dwindled, while interest on deposits has become a meaningful source of revenue. Robinhood’s Q3 earnings presentation calls this out.

In the interview with the WSJ, CEO Vlad Tenev also suggests a new push for Robinhood into retirement accounts, and into consumer credit via their acquisition of X1 for $104 million.

So, as a consumer, what’s the risk?

Investment accounts with Robinhood are covered by the Securities Investor Protection Corp. (SIPC). SIPC is similar to FDIC insurance and offers coverage of up to $500k in securities and cash held per brokerage account. If your accounts exceed that limit, the biggest risk to moving to Robinhood is belief in its ability to continue to operate. In the past year, Robinhood’s headcount has dwindled to 2,157 in Q3 ‘23 down from 3,416 in Q2 ‘22, following a series of layoffs.

Robinhood reported $94 billion in assets under custody at the end of November. In comparison, Schwab reported $8.2 trillion and Fidelity reported $11.5 trillion, both a whole order of magnitude larger than Robinhood. If Robinhood were to experience an SVB like situation, it’s pretty clear that they are not “too big to fail” and government agencies may not step in to make brokerage depositors whole.

Looking at Robinhood’s earnings statement, their Q3 ‘23 balance sheet held $5bn in corporate cash. Meanwhile, their quarterly net loss has oscillated wildly from $85mn to $511mn over the last few quarters. If their net loss continues to average $200-$300 mn, their corporate cash should be able to tide them over for the next few years.

That said, their earnings statement does call out: “A large portion of our revenue comes from interest income earned from our corporate cash and investment portfolio.” If interest rates drop in 2024 as is widely expected, Robinhood’s net loss is likely to widen further and the company does seem precariously positioned, with high sensitivity to interest rates.

In the end…

After weighing the risks, I decided that it was still worth the risk personally to take advantage of the offer. After resurrecting, my defunct Robinhood account, I was greeted by a prompt to transfer accounts in right on the homepage.

The flow to transfer in the assets was relatively painless — all that was needed was the account number from Schwab. Within 7 days, my assets were transferred retaining their cost basis from Schwab in Robinhood, with a couple1 of2 caveats3,

Within a couple of days of the transfer completing, the cash bonus was deposited in the brokerage account.

As a consumer, this bonus does seem to be a clear opportunity to take advantage of Robinhood’s corporate coffers. However, it’s worth doing so with a clear understanding of the risks, and motivations.

P.S. If you found this interesting, feel free to use my link to sign up.

P.P.S. Erm, why am I on this email?4

Robinhood does not support Joint Accounts, so the assets needed to be consolidated into a single individual account and moved over.

Robinhood does not have support for Treasury Bills and Mutual Funds.

The service that Robinhood uses to transfer accounts over (ACATS), unfortunately does not support transferring over fractional shares. The fractional shares are still held as-is in my original Schwab account.

I was inspired by a friend to start this Substack. In the early days of startups, there is often an opportunity for consumers to benefit from VCs or capital markets subsidizing businesses where the unit economics don’t entirely make sense. The goal of this substack is to identify these opportunities and help you capitalize on them.